Many MSME owners believe that the PMEGP loan is popular because it offers a low interest rate.

That belief is wrong — and this misunderstanding alone costs entrepreneurs lakhs of rupees in poor financial decisions.

The real strength of the PMEGP scheme lies not in lower interest rates, but in something far more powerful:

👉 Margin Money Subsidy

In this guide, we’ll explain PMEGP margin money subsidy in simple language, backed by official government guidelines, real examples, and practical MSME logic.

you may also like to read: How to Write a PMEGP Project Report That Gets Approved – Lessons From My Own Startup Journey

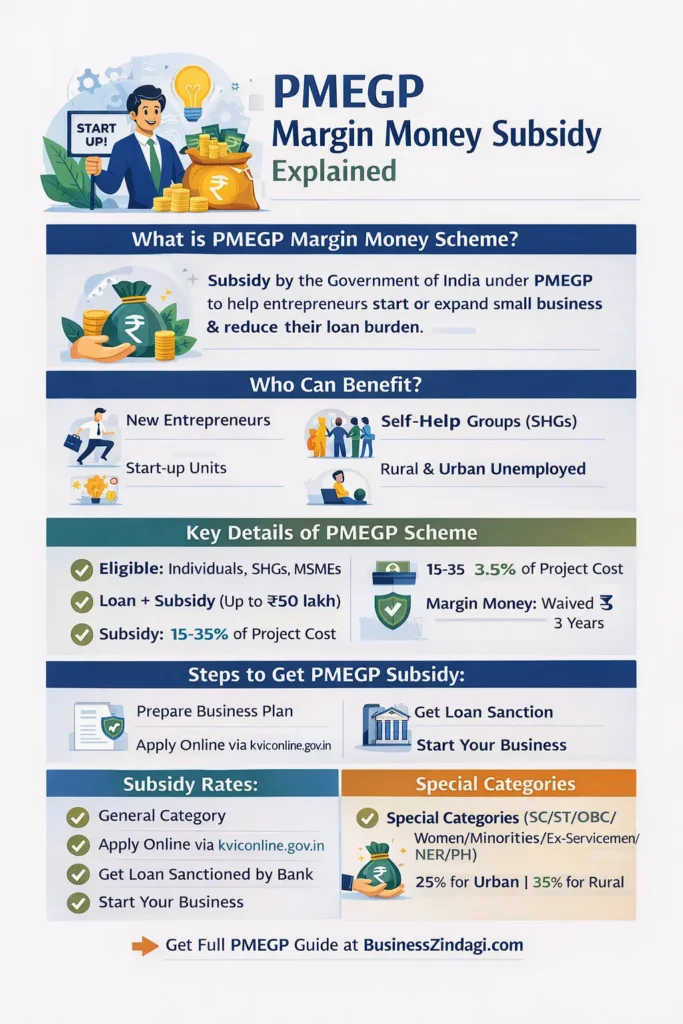

What Is PMEGP? (Quick Recap)

The Prime Minister’s Employment Generation Programme (PMEGP) is a government-backed credit-linked subsidy scheme launched in 2008 by the Ministry of MSME and implemented through KVIC, KVIBs, and District Industries Centres (DICs).

Its primary goal is to:

- Support first-time entrepreneurs

- Promote self-employment

- Encourage micro enterprises in manufacturing and services

related post: 10 Common Mistakes in PMEGP loan to Avoid While Applying.

Big Myth: PMEGP Offers Lower Interest Rates ❌

Let’s clear this upfront.

🔴 PMEGP does NOT provide a fixed or concessional interest rate.

According to official PMEGP guidelines:

Banks are free to charge their normal MSME lending rate on PMEGP loans.

This means:

- Interest rate varies from bank to bank

- It also depends on time, loan size, and credit policy

- There is no special PMEGP interest rate chart

So why is PMEGP still considered attractive?

you may also like to read:Affordable Finance for Entrepreneurs: How the Prime Minister’s Employment Generation Programme (PMEGP) is Empowering First-Generation Business Owners

The Real Benefit: What Is Margin Money Subsidy in PMEGP? ✅

Margin money subsidy is the amount the government contributes to your project cost, so you don’t have to borrow that portion from the bank.

This subsidy:

- Is credited upfront

- Is not repayable

- Carries zero interest

- Reduces your loan burden from day one

Margin Money Subsidy Rates

| Category | Urban Area | Rural Area |

|---|---|---|

| General | 15% | 25% |

| SC / ST / OBC / Minority / Women / Ex-Servicemen | 25% | 35% |

Simple Example: How Margin Money Saves You Lakhs

Let’s say you apply for PMEGP with a ₹10 lakh project.

- Government subsidy (35%) → ₹3.5 lakh

- Bank loan ➝ ₹6.5 lakh

- Interest charged only on ➝ ₹6.5 lakh

💡 You never pay interest on ₹3.5 lakh. Ever.

This is the hidden saving most MSMEs completely miss.

Why PMEGP Is Cheaper Even With Normal Interest Rates

Even if a bank charges 11–12% interest:

- EMI is lower

- Total interest paid over loan tenure is lower

- Financial pressure in early years reduces

PMEGP vs Normal MSME Loan

| Feature | PMEGP Loan | Regular MSME Loan |

|---|---|---|

| Interest rate | Bank MSME rate | Bank MSME rate |

| Government subsidy | ✅ Yes | ❌ No |

| Interest on subsidy | ❌ Not charged | NA |

| Loan burden | Lower | Higher |

| First-time entrepreneur friendly | ✅ Yes | ❌ Often difficult |

Is There Any Interest Subsidy in PMEGP?

✅ Direct interest subsidy under PMEGP? → NO

✅ Indirect benefit? → YES

Here’s how:

- Margin money is kept separate (often locked for 3 years)

- That portion is interest-free

- You pay interest only on bank-financed portion

Special Case: 2018–2021 MSME Interest Subvention

Between 2018 and March 2021, the Government of India ran a 2% Interest Subvention Scheme for MSMEs.

If a PMEGP borrower:

- Was GST-registered

- Took eligible incremental credit

they may have received 2% interest relief.

⛔ This scheme is now discontinued.

PMEGP Interest Rate History Since Launch (2008)

Here’s the honest truth many sites won’t tell you:

- PMEGP never had a fixed interest rate

- Since 2008, banks have always applied prevailing MSME lending rates

- Rates generally ranged between 10%–13% depending on time & bank policy

- Government never published a year-wise PMEGP interest rate chart (because it doesn’t exist)

👉 Margin money subsidy has always been the core benefit, not interest control.

Maximum Interest Charged on PMEGP: What You Should Know

There is no official “maximum PMEGP interest rate”, but:

- Banks cannot charge arbitrary rates

- RBI MSME lending norms apply

- Rates must be disclosed in sanction letter

💡 Tip: Always compare PMEGP sanction rate with:

- MUDRA loan

- Regular MSME term loan

Why Margin Money Matters So Much for MSMEs

For small businesses:

- Cash flow is fragile

- Initial years decide survival

- High EMI kills growth

Margin money:

✅ Reduces risk

✅ Improves viability

✅ Encourages formal entrepreneurship

This is why PMEGP is not a cheap loan — it’s a smarter loan.

FAQs on PMEGP Margin Money Subsidy

Q1. Is PMEGP subsidy refundable?

No. It is a government grant, not a loan.

Q2. Will bank deduct subsidy from my loan?

Yes. Loan is calculated after subsidy adjustment.

Q3. Is interest charged on subsidy amount?

No. Zero interest.

Q4. Can banks refuse PMEGP due to low interest rates?

Banks don’t bear subsidy cost, so interest rate is not a loss to them.

Final Verdict (BusinessZindagi Insight)

PMEGP is not about paying less interest per year.

It’s about borrowing less money and paying less interest overall.

Entrepreneurs who understand margin money:

- Plan better

- Borrow smarter

- Grow faster

Those who chase “cheap interest” often miss the bigger picture.

Disclaimer

PMEGP guidelines, subsidy rates, and interest policies are subject to change as per Government of India and bank norms. Interest rates vary by bank and time. Always verify details from official KVIC / MSME portals or your lending bank.

About the Author

BusinessZindagi focuses on practical MSME knowledge, government schemes explained in simple language, and real-world business insights for Indian entrepreneurs.

✅ Official References & Authentic Links

- Ministry of MSME – PMEGP Scheme Overview

https://msme.gov.in/schemes/prime-ministers-employment-generation-programme - KVIC – PMEGP Official Portal

https://www.kviconline.gov.in/pmegpeportal - PMEGP Applicant FAQs (Subsidy, Eligibility, Process)

https://www.kviconline.gov.in/pmegpeportal/jsp/SchemeFaqApplicant.html - PMEGP Scheme Guidelines (Official PDF)

https://www.kviconline.gov.in/pmegp/pmegpweb/docs/pdf/PMEGPscheme.pdf - Revised PMEGP Guidelines (Latest – 2023)

https://www.kviconline.gov.in/pmegpeportal/dashboard/notification/Revised_PMEGP_Scheme_Guidelines_07122023.pdf - Udyam Registration (Mandatory for MSMEs)

https://udyamregistration.gov.in